Suppose a number of otherwise identical countries differ in endowments of factors of production. And suppose these countries do not permit trade in factors of production among themselves. For example, workers are not permitted to emigrate from one country and into another. And capitalists cannot invest in foreign countries. But suppose all produced commodities can be traded among these countries on an international market. Then, according to many counfused mainstream economists, the prices of the factors of production will tend towards equality among these countries. For example, the wage will be the same everywhere. In some sense, trade in produced commodities can replace trade in factors of production. If these countries were to allow foreign investment, after trade in produced commodities had already been established, then, according to these confused mainstream economists, the same equilibrium would only be achieved quicker. I expect these confused mainstream economists would qualify this story in practice by relating wages to variations in productivity among countries no longer considered identical, transportation costs, etc.

The above story relies on the factor price theorem, which is most conveniently set out in the case where only two countries exist. This supposed theorem has some conditions, and all these conditions are met by the Mainwaring example being analyzed in this series of posts:

- Both countries produce the same commodities. In this case, the commodities consist of iron, steel, and corn.

- Each country has a given endowment of factors, identical in quality but of different relative quantities. For my purposes, I do not need to specify explicitly the quantity of labor available in each country nor to discuss the endowment of the value of capital.

- Both countries have identical technology.

- There are no factor reversals. I rely on Mainwaring for the truth of this assumption in this case. I have neither checked it nor fully attempted to understand its statement.

- All consumers have identical and homothetic utility functions. As with the assumption on endowments, my purposes do not require an explicit specification of utility functions.

- All commodities that can enter into final output are traded on international markets in which one price rules for each commodity. In this case, the prices of iron, steel, and corn are established on international markets.

- There are no transportation costs.

- Perfect competition prevails in all markets.

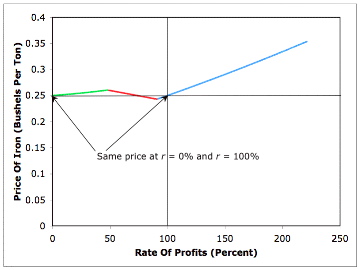

"From the price equations it is clear that a set of product prices implies a particular wage and rate of interest. For factor price equalization it is critical to investigate the conditions necessary for this to be a one-to-one relationship, so that a common set of product prices in any two countries will necessarily be associated with same wage and interest rate." - Keith Acheson (1970)In two previous posts, I worked through the analysis of the choice of technique in a three commodity example created by Lynn Mainwaring. Figure 4-1 shows the price of iron at all feasible levels of the rate of profits in this example. Figure 4-2 shows the corresponding price of steel. I have picked out the prices at two rates of profits in the figure. These points are further detailed in Table 4-1. Suppose the prices on the international markets for iron, steel, and corn are 1/4 bushels per ton iron, 1/2 bushels per ton steel, and unity (by definition), respectively. Let the wage in the first country be three bushels corn per person year and the rate of profits be 0%. Let the wage in the second country be one bushel per person year and the rate of profits be 100%. The analysis of the choice of technique shows that this is an equilibrium.

|

|---|

| Figure 4-1: The Price Of Iron |

|

|---|

| Figure 4-2: The Price Of Steel |

| p1 = 1/4, p2 = 1/2, r = 0%, w = 3, Delta technique adopted |

| p1 = 1/4, p2 = 1/2, r = 100%, w = 1, Alpha technique adopted |

Thus, in Mainwaring's example an equilibrium exists in which:

- There is one price on the international market of each produced commodity.

- The wage and the return to financial capital differ between countries.

5.0 Conclusion

So that's the theory at a very abstract level. If a country trades produced goods on "free" markets, opening its financial markets to international investors can dramatically change the dynamics of income distribution, or so the theory suggests. As I understand it, mainstream economists, who often get their sums wrong, think the theory implies opening financial markets will only lead to equilibrium with common factor prices, perhaps corrected for differences in productivity, transport costs, and so on, being established quicker.

Why do mainstream economists continue to teach and to try to apply theories show to be false more than a generation ago?

References

- Acheson, K. (1970). "The Aggregation of Heterogeneous Capital Goods and Various Trade Theorems", Journal of Political Economy, V. 78, N. 3 (May-June): 565-571.

- Mainwaring, L. (1976). "Relative Prices and 'Factor Price' Equalisation in a Heterogeneous Capital Goods Model", Australian Economic Papers, Republished in Fundamental Issues in Trade Theory (Ed. by Ian Steedman), Macmillan, 1979.

No comments:

Post a Comment